| |

|

Accounting records that are not maintained according to the

Double Entry System are known as Accounts from Incomplete Records or Single

Entry System of Accounting. It is an incomplete double entry system varying

with circumstances.

Key Points:

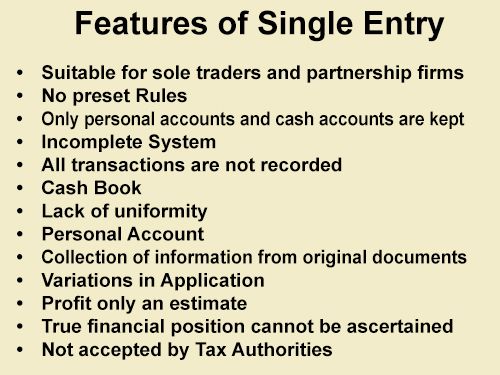

· Incomplete Records: It is a system of recording business transactions. In some of the transactions, both aspects are recorded; while in other on aspect is recorded or it is not recorded at all.

· Statements of Affairs: It is a statement of Assets and Liabilities. The difference between the two sides represents the proprietor’s (owner) capital.

· Capital: Amount invested by the owner.

· Drawings: Money or goods taken by the proprietor from the business for his/her personal use.

· Incomplete Records: It is a system of recording business transactions. In some of the transactions, both aspects are recorded; while in other on aspect is recorded or it is not recorded at all.

· Statements of Affairs: It is a statement of Assets and Liabilities. The difference between the two sides represents the proprietor’s (owner) capital.

· Capital: Amount invested by the owner.

· Drawings: Money or goods taken by the proprietor from the business for his/her personal use.

Ascertaining Profit under the Single Entry System:

1. Statements of Affairs Method

2. Conversion method

Net Worth Method or Statement of Affairs

Method

A Statements of Affairs is a statement of

assets and liabilities. Difference between the amounts of the two sides is

taken as capital method. Under the Single Entry System, it is necessary to

prepare Statements of Affairs at the

end of the year and also in the beginning of the year, if not already prepared

to determine profit. However, following two adjustments must be borne in mind

for determining profit:

·

Adjustment

for Capital Introduced: If the proprietor bought in additional capital

during the year, it should be deducted from the capital at the end (since this

increase is not due to profit but fresh introduction of capital).

·

Adjustments

for drawings: Drawings by the proprietor should be added to the capital at

the end and had the drawings not been made, the capital at the close of the

year would have been higher.

Formula for determining the profit is as

follows:

Profit = Capital at the end + Drawings – Additional Capital Introduced –

Capital in the beginning.

The above

formula may be shown as follows in the form of Statement of Profit or Loss:

Statement of Profit or Loss

For the year ended…

Example1: Akansha maintains books on

Single Entry System. She gives you the following information:

|

Particulars

|

Amount (Rs.)

|

|

Capital at the end

Add:

Drawings during the year

Less: Additional

Capital Introduced during the year

Adjusted capital at

the end

Less:

Capital in the beginning

Profit or Loss for the year

|

xxx

xxx

|

|

xxx

xxx

|

|

|

xxx

xxx

|

|

|

xxx

|

Capital on 1st April, 2018 Rs. 30,400

Capital on 1st April, 2019 Rs. 33,800

Drawings made during the period: April, 2018 to

March,2019 Rs. 9,600

Capital introduced on 1st August,2018 Rs. 4,000

You are

required to calculate the profit or loss made by Akansha.

Statement of Profit or Loss

For the year ended 31st

March,2019

Example2: Calculate the amount of profit or loss of Mr. X:

|

Particulars

|

Amount (Rs.)

|

|

Capital as on 1st

April, 2019

Add:

Drawings during the year: April,2018 to March,2019

Less:

Capital Introduced on 1st August,2018

Adjusted capital on

1st April,2019

Less:

Capital on 1st April,2018

Profit made during the year

|

33,800

9,600

|

|

43,400

4,000

|

|

|

39,400

30,400

|

|

|

9,000

|

Example2: Calculate the amount of profit or loss of Mr. X:

|

Particulars

|

Amount (Rs.)

1st Jan,2018

|

Amount (Rs.)

31st Dec,2018

|

|

Cash

Bank

Furniture

Creditor

Outstanding

Expenses

Stock

|

10,000

5,000

50,000

10,000

5,000

13,000

|

25,000

30,000

7,000

13,000

7,000

52,000

|

Solution:

Statement of Profit or Loss

For the year ended 31st Dec, 2018

Working

notes:

|

Particulars

|

Amount (Rs.)

|

|

Closing capital

Opening capital

Drawings

|

94,000

(63,000)

40,000

|

|

Net Profit

|

71,000

|

Statement of Affairs as at 31st Dec, 2018

Balance Sheet as on 31st Dec, 2018

|

Liabilities

|

Amount

(Rs.)

|

Assets

|

Amount

(Rs.)

|

|

Capital (b/f)

Creditor

Outstanding expenses

|

94,000

13,000

7,000

|

Cash

Bank

Furniture

Stock

|

25,000

30,000

7,000

52,000

|

|

|

1,14,000

|

|

1,14,000

|

|

Liabilities

|

Amount

(Rs.)

|

Assets

|

Amount

(Rs.)

|

|

Capital (b/f)

Creditor

|

63,000

10,000

|

Cash

Bank

Furniture

Stock

|

10,000

5,000

50,000

13,000

|

|

|

73,000

|

|

73,000

|

Informative.

ReplyDeleteInformative content

ReplyDelete